Subtotal $0.00

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by Themiya

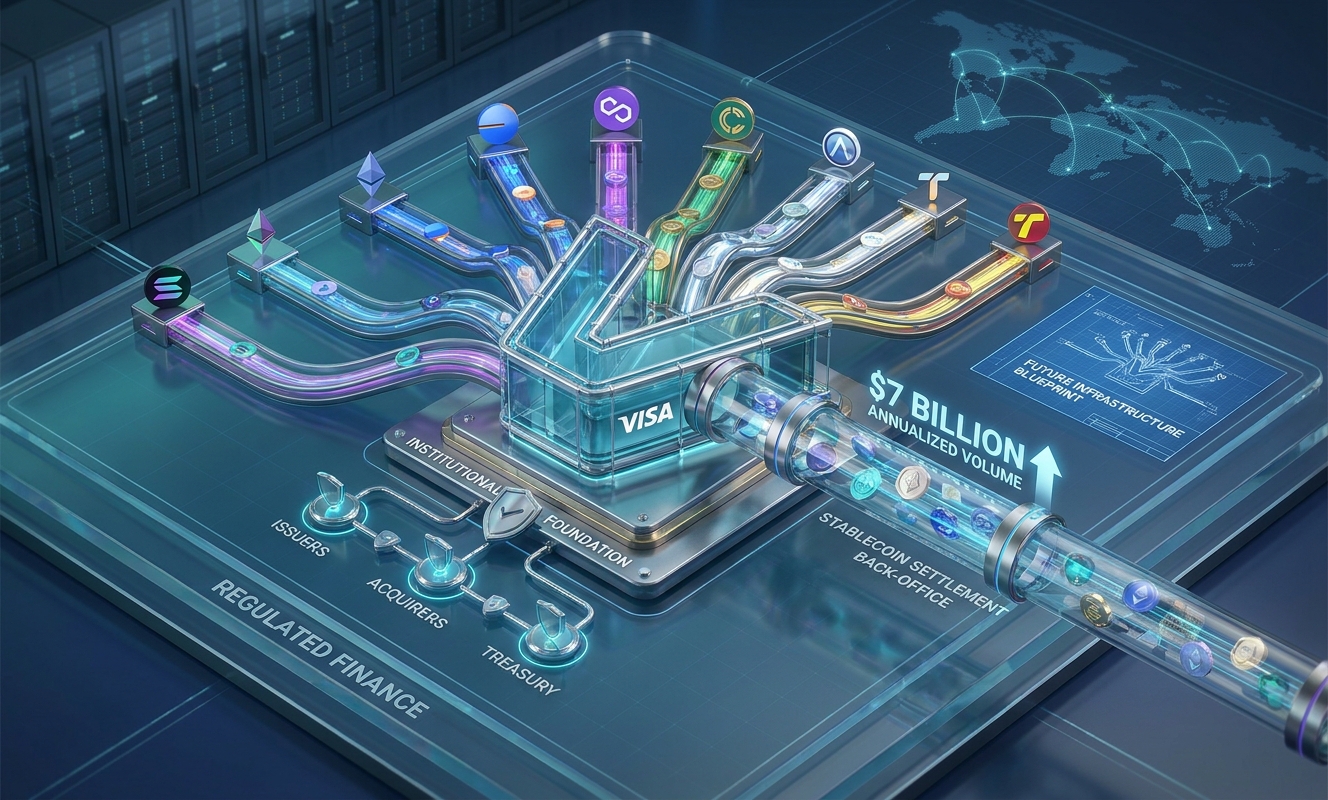

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by ThemiyaThe checkout screen looks the same. Your card gets swiped, you get a receipt, and you move on. But somewhere in the plumbing beneath that transaction, Visa just ran $7 billion in stablecoin settlement volume, annualized, across nine blockchains. And the number grew 50% in a single quarter. Let that sit for a second.

Let’s be real about what’s happening here. Visa isn’t adding stablecoins to its app or launching a new crypto card for retail hype. They’re rerouting the part of payments that consumers never see. We’re talking about the settlement layer. The part where your issuing bank and the merchant’s acquiring bank square up after the transaction is already done.

That’s the unsexy, boring, critical infrastructure where trillions of dollars move every single year. And Visa just ran a sizable chunk of it over USDC on Solana, Ethereum, Base, Polygon and four other chains.

Here’s the thing. The real signal isn’t the blockchain count. It’s the direction of travel.

This isn’t a proof of concept anymore. It’s a product in production.

The chain selection is not random. Every addition tells you something about who Visa is building for. Ignore the marketing, look at the function.

Canton is on this list for one reason. Regulated financial institutions will never run settlement over a fully transparent public ledger where counterparties, amounts, and treasury strategies are visible to any node operator paying attention. Canton gives banks need-to-know privacy on a public blockchain. Visa becoming a Canton Super Validator in March 2026 wasn’t a side project. It was a deliberate move to keep regulated finance inside the tent.

Base is here because Coinbase controls the on-ramp for tens of millions of U.S. retail crypto holders. Low gas, USDC-native settlement, wallet connectivity baked in. Adding Base is Visa telling program managers: your end users can fund from a Coinbase account and we’ll handle the settlement side. That’s not blockchain ideology. That’s distribution strategy.

Arc is Circle’s own Layer 1. Sub-second finality, USDC-denominated fees, predictable costs. Honestly, adding Arc to Visa’s rails is basically a Circle-Visa vertical integration in slow motion. Watch that relationship carefully over the next 12 months.

Polygon and Tempo round out the roster. Lower-cost transactions with Polygon’s existing stablecoin liquidity. Tempo brings dedicated payment lanes and payment metadata for reconciliation, which matters deeply to treasury teams who need to match settlements to invoices. That’s a boring detail that signals serious production intent.

Look, most of crypto Twitter will frame this as a bullish signal for SOL, ETH, and MATIC. And sure, more institutional settlement volume running over these networks is not a bad thing for fee revenue and on-chain activity. But let’s put on the skeptical lens here.

The real beneficiaries in the market, if you’re thinking about this correctly, are the infrastructure layers. Solana for throughput. Ethereum as the base layer of trust. Polygon for cost-sensitive volume. And Circle, which remains a private company sitting at the absolute center of this entire architecture. That IPO, when it comes, will be priced with this kind of data on the slide deck.

Visa has been extremely careful with its language here. And honestly, that’s worth respecting rather than dismissing. They’ve given us a run rate but zero breakdown by chain, geography, partner, or stablecoin type. We don’t know if 80% of that $7 billion is running over one chain with eight others barely active. We don’t know which acquirers or issuers are actually live versus just “supported.”

Between you and me, that opacity is doing a lot of work. A $7 billion annualized run rate sounds massive until you remember that VisaNet processes around $15 trillion a year in payment volume. The stablecoin settlement pilot represents something well under 0.1% of Visa’s actual throughput. The infrastructure is real. The scale is still tiny.

The word “pilot” is load-bearing here. It gives Visa the ability to expand aggressively if regulatory winds cooperate, or to quietly scale back if something goes wrong, without ever having committed to a production timeline.

If you’re trying to position around this trend intelligently, here’s the framework I’d use.

The back office is being rebuilt in real time. Consumers won’t notice until it’s already done. That’s exactly how the most consequential infrastructure shifts always happen.

References & Sources:

While Visa is quietly upgrading global payment rails with stablecoins, traditional banking institutions are also making major moves to build out mainstream digital financial plumbing. A consortium of nine major European banks—Banca Sella, CaixaBank, Danske Bank, DekaBank, ING, KBC, Raiffeisen Bank International, SEB, and UniCredit—has joined forces to launch a joint venture known as Qivalis. Regulated under the Dutch Central Bank (DNB), this initiative aims to issue a MiCAR-compliant euro-pegged stablecoin. This collaborative effort highlights a massive, industry-wide shift where both legacy banks and payment giants are integrating digital currencies directly into everyday financial infrastructure.

Visa is primarily using USD Coin (USDC) to upgrade its payment infrastructure. By becoming the first major payments network to directly settle transactions in USDC, Visa is forging a vital new connection between traditional fiat currencies and digital assets. Behind the scenes, Visa uses this fully backed, US dollar-pegged stablecoin to settle obligations with crypto-native partners over blockchain networks like Ethereum and Solana. This means Visa is quietly processing everyday transactions using crypto rails without consumers ever needing to change how they swipe their cards.

Visa is strategically embedding stablecoins into its backend plumbing to future-proof its network and dominate the next era of global finance. Stablecoins are heavily utilized for international transfers, cross-border commerce, and remittances. By settling transactions with stablecoins instead of traditional fiat currencies, Visa can drastically accelerate settlement times, bypass cumbersome traditional banking hours, and reduce foreign exchange (FX) friction. Ultimately, this allows Visa to offer cheaper, faster cross-border payments, keeping this massive transaction flow on its own network rather than losing it to blockchain-only payment alternatives.

Yes, Visa is rapidly expanding its digital currency transaction capabilities. The payment giant recently announced that it has added support for four new stablecoins distributed across four different blockchains. This multi-chain, multi-token approach reveals Visa’s quiet but aggressive strategy to build a highly adaptable, blockchain-agnostic payment infrastructure. By supporting a wider variety of stablecoins beyond just USDC, Visa ensures that its mainstream payment plumbing can seamlessly route digital money across the globe, accommodating the diverse needs of financial institutions, merchants, and consumers.