Subtotal $0.00

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

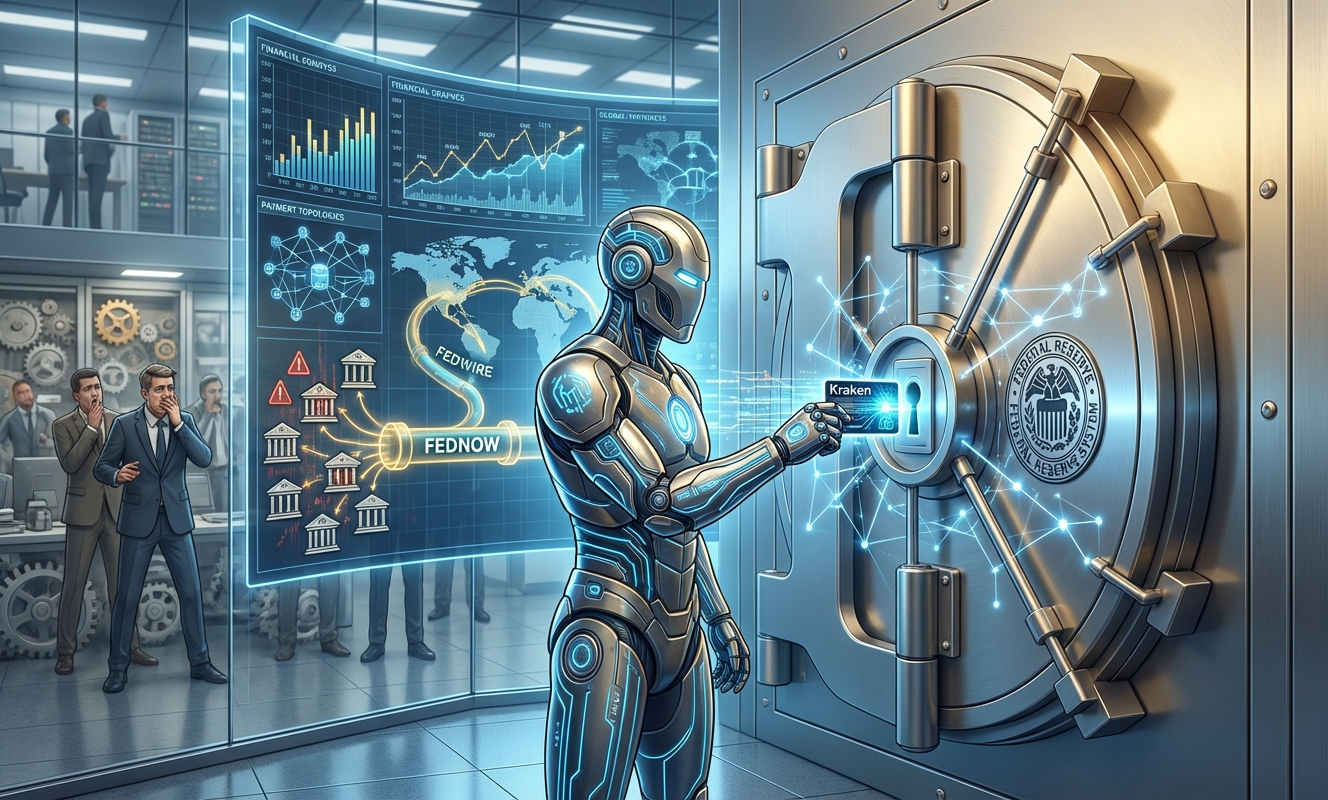

Kraken didn’t just win a regulatory approval. It quietly rewired its competitive position in a way most of the industry hasn’t fully processed yet. On March 4, 2026, Kraken Financial, its Wyoming-chartered bank, became one of the first crypto-native institutions to receive a Federal Reserve master account. That means direct settlement over Fed rails. No middlemen. No sponsor bank holding the keys to your dollar pipeline.

This is a big deal. Let’s actually break down why.

Here’s the thing most retail traders completely miss. Every time you deposit USD onto a crypto exchange, that money doesn’t travel through some sleek, proprietary system. It crawls through a patchwork of sponsor banks, institutions that have quietly held enormous power over the entire industry for years.

And those sponsor banks? They can pull the plug whenever it’s politically convenient for them. We’ve seen it happen. During periods of regulatory heat, exchanges lose banking access almost overnight. Customers are stuck. Withdrawals get delayed. The whole “be your own bank” narrative collapses the second a mid-sized bank in Kansas decides crypto is too hot to handle.

Kraken just severed that dependency. Almost entirely.

With a Fed master account, Kraken Financial can now settle US dollar payments directly over Fedwire Funds and FedNow. No sponsor bank sitting in between, taking its cut and holding a kill switch over Kraken’s dollar operations. That’s not a minor operational upgrade. That is a structural shift in how much counterparty risk Kraken carries.

Let’s be real. The Fed doesn’t hand out master accounts to crypto companies out of the goodness of its heart. This approval happened because it serves a very specific policy agenda.

The Federal Reserve has been quietly designing a narrower form of central bank access called a “Payment Account,” a prototype it put out for public comment in December 2025. The concept is simple on the surface. Give certain non-traditional institutions access to settlement infrastructure, but strip out the full safety net. No interest on balances. No discount window access. No intraday credit. An overnight balance cap set at the lower of $500 million or 10% of total assets.

Kraken’s one-year, limited-purpose account isn’t really a full master account in the traditional sense. It looks a lot more like a live beta test for that Payment Account concept. The Fed needed a real-world guinea pig with enough compliance infrastructure to make the experiment credible. Kraken, operating through a Wyoming Special Purpose Depository Institution (SPDI) charter, which is fully reserved and prohibited from lending customer deposits, fit the profile.

Kansas City Fed President Jeff Schmid described it in careful, measured terms. “The integrity and stability of the US payments system remain our priority.” Translation: we’re opening a small door, we’re watching every inch of what walks through it, and we reserve the right to slam it shut.

The SPDI structure matters here more than the headlines suggest. Wyoming designed SPDIs to be fully reserved, meaning Kraken Financial can’t play the fractional reserve game traditional banks run. Every customer dollar on deposit is backed one-to-one. That eliminates the classic bank-run risk and maturity-mismatch problem that makes regulators nervous about extending Fed access to new institution types.

That’s the specific reason this approval was possible. Kraken didn’t just lobby its way in. It built a regulatory structure that gave the Fed a defensible reason to say yes without setting a precedent it would immediately regret.

Short answer: it’s enormous. And it creates a moat that most competitors can’t replicate quickly.

Co-CEO Arjun Sethi talked about atomic settlement between fiat and crypto, institutional-grade cash management integrated with digital asset custody, and programmable financial products inside a fully regulated framework. That’s not corporate fluff. Those are real product categories that institutional clients have been asking for and not getting from crypto-native firms.

Here’s the uncomfortable truth for the rest of the industry. This approval is going to deepen the divide between regulated infrastructure players and everyone else.

The firms that can absorb the compliance cost of bank-level regulation, governance structures, and Fed supervisory requirements will be able to internalize their payments stack. The firms that can’t will keep depending on sponsor banks and keep absorbing the operational and political risk that comes with that dependency.

Think about what that means in practice. If Coinbase, Gemini, or any other major exchange suffers a banking disruption while Kraken’s dollar rails stay live and operational, the institutional client exodus will be swift and merciless. Institutions don’t tolerate payment uncertainty. They just move to whoever doesn’t have it.

Regulation, in this case, isn’t the obstacle. It’s the product.

Don’t expect a linear rollout. There are three plausible paths from here, and the market is pricing in exactly none of them with any nuance.

Honestly, the direct price impact on BTC is not the story here. This isn’t a catalyst for a short-term pump. It’s a slower-burning structural shift with medium-term implications.

What it does signal, clearly, is that the on-ramp and off-ramp infrastructure connecting crypto markets to the US dollar system is being quietly hardened. That matters for sustained institutional capital flows. Institutional money doesn’t pour into markets where dollar access is fragile and dependent on a bank’s mood. When the plumbing gets more reliable, the water flows more consistently.

For KRAK (if Kraken eventually goes public or its implied valuation is part of your thesis), this is a genuine fundamental positive. For the broader market, it’s a signal that crypto is being integrated into core financial infrastructure in a way that’s harder to reverse than any single regulatory policy decision.

Watch how Coinbase responds. If they accelerate efforts to deepen their own banking charter activity, you’ll know they’ve read this development correctly.

This approval is structured as a limited-purpose, one-year term. That is not a permanent seat at the table. It is a probationary period with full Fed supervisory eyes on every transaction.

Don’t buy Kraken’s competitive advantage without stress-testing the assumptions. Here’s what to actually watch:

The machinery of US dollar settlement just let a crypto company touch the controls. For a year. Under close supervision. With strict limits. But it happened. And in this industry, the first approval is almost always the one that gets remembered.

Kraken as a whole is not shutting down; in fact, it is expanding rapidly, having recently secured rare Federal Reserve access. The confusion stems from Kraken’s decision to close its NFT marketplace. The company chose to wind down the NFT platform to strategically shift its resources toward new products, services, and structural expansions—such as leveraging its new banking capabilities to bridge traditional finance and crypto.

Yes, Kraken is widely recognized as a safe, highly established cryptocurrency exchange equipped with robust security measures. Its recent milestone of gaining direct access to the Federal Reserve further cements its regulatory legitimacy and institutional strength. To maximize your account safety, always use a unique, strong password and enable two-factor authentication (2FA). However, while Kraken is secure for active trading, experts generally recommend transferring long-term cryptocurrency holdings to a personal hardware wallet for maximum security.

No, Kraken is not a Chinese company. Legally known as Payward, Inc., Kraken is a strictly US-based cryptocurrency exchange that was founded in 2011. Its deep regulatory roots in the United States are highlighted by its recent, industry-leading achievement of securing a Federal Reserve master account through its Wyoming bank charter, which deeply integrates the exchange into the traditional American financial system.

Cryptocurrency platforms and fintechs pursue US bank charters to gain financial independence, regulatory clarity, and stability. A charter allows these companies to operate under a single federal regulator instead of navigating a complex, expensive state-by-state licensing system. Most importantly, it grants direct, durable access to the Federal Reserve. As seen with Kraken’s recent Federal Reserve access, this eliminates the need to rely on fragile third-party sponsor banks, allowing the exchange to directly process fiat transactions, reduce funding costs, and offer highly secure services to its users.