Subtotal $0.00

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by Themiya

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by ThemiyaThe stablecoin market just crossed $315 billion. And the conversation everyone’s having about it is wrong.

Most analysts are still fixated on the supply leaderboard. Tether leads. Circle trails. End of story. But that framing misses the actual fight, which isn’t about who has the biggest pile of digital dollars parked on Binance. It’s about who controls the pipes and rails that the next trillion dollars of institutional money flows through. That’s a fundamentally different contest. And right now, Circle is quietly winning it.

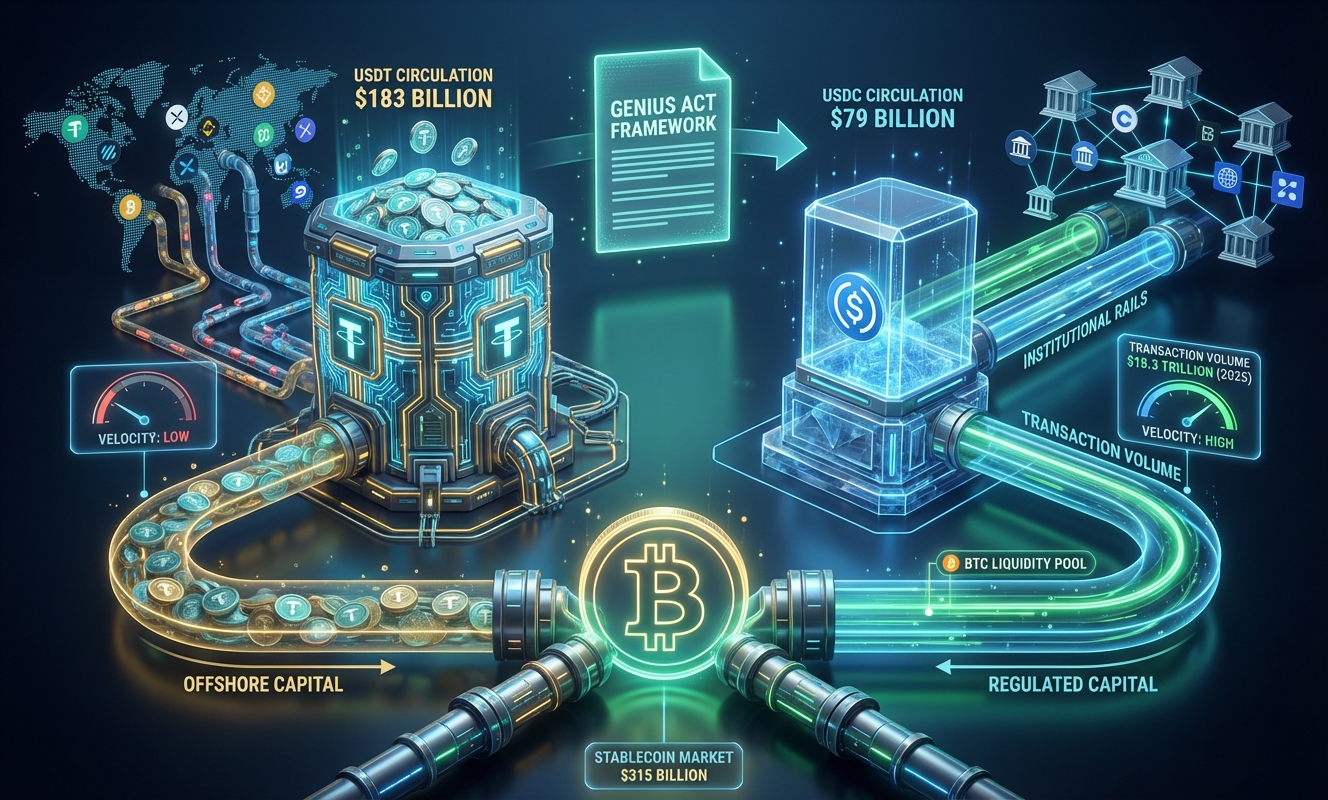

Let’s be real about what the raw numbers say. USDT circulation is sitting at approximately $183 billion. USDC is at $79 billion. On the surface, Tether wins by a landslide. But here’s the thing: supply tells you where money is sleeping. Velocity tells you where money is working.

Bloomberg, citing Artemis Analytics, reported total stablecoin transaction volume hit $33 trillion in 2025. A 72% jump year over year. Now look at who drove it.

Read that again. USDC, which holds less than half of USDT’s supply, processed more dollars in actual transactions. That’s not a minor footnote. That’s a fundamental signal about which token is becoming the preferred medium for moving money, not just storing it. Circle also reported USDC Q4 on-chain transaction volume alone hit $12 trillion, up 247% year over year. That’s not organic growth. That’s institutional adoption kicking into a higher gear.

Tether, meanwhile, is still sitting roughly $3 billion below the all-time supply peak it hit in December 2025. Not collapsing by any means. But not accelerating either.

Honestly, both of these companies made rational strategic bets. They just chose completely different terrains to win on.

Tether built its dominance on distribution. Deep exchange integrations, offshore trading venues, and emerging markets where people need a dollar-linked asset precisely because their local currency is getting wrecked or their banks are useless. That’s a real, durable moat. It’s the reason USDT still accounts for 58% of the entire stablecoin market by supply. You don’t build that kind of footprint by accident.

But Tether’s reserve transparency has always been its Achilles heel. S&P downgraded it. Regulators have questioned it for years. And the USDT audit situation is still unresolved, even after Tether brought on Deloitte as auditor for its newer US stablecoin product. USDT itself? Still not included. That’s a detail worth remembering.

Circle went the other direction entirely. The company built USDC on legibility. Its reserves sit primarily in the BlackRock-managed Circle Reserve Fund, with the rest in cash at regulated financial institutions. Deloitte audits its financial statements. Monthly disclosures. Clean compliance architecture. It’s built for the kind of institutions that have legal and compliance teams who need to sign off on every counterparty.

Look, neither model is wrong. But the regulatory winds are clearly blowing in one direction.

The policy backdrop is shifting in ways most retail traders aren’t tracking. The GENIUS Act framework, reviewed by the Federal Reserve Bank of St. Louis, establishes that payment stablecoin issuers above $50 billion in circulation face tight reserve requirements, mandatory monthly disclosures, and annual audited financial statements. State-qualified issuers above $10 billion face a hard deadline to transition toward federal oversight within a year.

These thresholds aren’t just regulatory compliance boxes. They’re a structural filter. And Circle, with its existing Deloitte relationship, BlackRock reserve fund, and transparent disclosure framework, is already sitting inside that filter. Comfortably.

Tether, operating primarily offshore and without a full USDT audit from a Big Four firm, has more friction to clear. That doesn’t mean it’s finished. But it does mean the next wave of regulated capital, the banks, the payment processors, the treasury desks, will almost certainly default to USDC as their stablecoin of choice.

Visa already made that call. They launched USDC settlement in the US with Cross River Bank and Lead Bank, and their monthly stablecoin settlement volume was running at a $3.5 billion annualized rate as of late November. That’s not a pilot program anymore. That’s infrastructure being laid.

Here’s where it gets directly relevant for anyone holding BTC.

Stablecoins are the lifeblood of crypto liquidity. They fund exchange balances, back collateral positions, and let traders rotate into Bitcoin without touching a bank wire. When stablecoin supply expands, the pool of deployable dollar liquidity inside crypto deepens. That buying power has to go somewhere. Historically, a significant chunk of it finds its way into Bitcoin.

Glassnode’s Stablecoin Supply Ratio frames it well: lower ratios imply greater stablecoin-denominated purchasing power relative to Bitcoin supply. More stablecoin capital waiting on the sidelines means a bigger potential bid for BTC.

The emerging reality, though, is that Bitcoin liquidity could become more segmented over the next 12 to 18 months. Two distinct pools.

Standard Chartered projects the stablecoin market could hit $2 trillion by end of 2028. From today’s $315 billion base, that’s roughly $1.7 trillion in new stablecoin capital entering the ecosystem. The critical question for every Bitcoin investor isn’t who wins the current supply race. It’s which issuer captures more of that incoming $1.7 trillion.

Before we get to the risk factors, here’s the split laid out cleanly:

The momentum divergence is real. It’s not dramatic enough to call this an imminent overthrow. But it’s consistent enough to take seriously.

Between you and me, there’s a trap here that a lot of analysts are walking into. They see USDC’s transaction velocity lead, its regulatory alignment, and its institutional integrations and immediately project a clean Tether takeover. That’s probably wrong, at least in the near term.

Tether’s distribution moat is genuinely hard to replicate. The majority of the world’s crypto trading volume still settles in USDT. Emerging market users who rely on USDT for dollar access don’t care about Deloitte audits. They care about liquidity, accessibility, and the fact that USDT is available on every exchange in existence. That user base isn’t migrating to USDC because of a favorable regulatory framework in Washington.

Consider these specific risks before adjusting your positioning based on this narrative:

If you’re a Bitcoin holder watching this play out, here’s how to think about it practically.

The stablecoin supply race is largely a vanity metric for your purposes. What matters for BTC price action is whether new dollar liquidity is entering the crypto ecosystem and finding its way to Bitcoin. Both USDT expansion and USDC expansion contribute to that. A growing stablecoin market, regardless of which issuer leads, is generally a positive leading indicator for Bitcoin demand.

The more interesting trade is paying attention to which venues are integrating USDC at scale. Visa’s settlement integration is the most visible example right now. As more traditional financial infrastructure adopts USDC natively, it lowers the friction for institutional BTC purchases routed through compliant channels. That’s a structural tailwind for Bitcoin that compounds over time.

Watch the USDC market cap as a forward indicator. When USDC supply is growing fast and consistently, it signals that regulated, compliance-focused capital is actively entering the crypto ecosystem. Historically, that type of capital flows toward Bitcoin first. The 72% year-over-year USDC circulation growth we saw in 2025 is exactly the kind of number that should be on your radar.

Don’t pick a side in the Tether vs. Circle debate. Use both data sets to track where the money is and where it’s going. That’s the actual edge here.

References & Sources:

Circle’s USDC and Tether’s USDT are both stablecoins pegged to the US dollar, but they differ primarily in regulatory transparency and reserve backing. Circle is widely recognized for its strict US regulatory compliance, monthly attestations, and holding reserves strictly in cash and short-term US Treasuries. Tether, while historically the market leader, has faced regulatory scrutiny regarding the exact composition of its commercial paper and asset reserves. As the market increasingly demands compliance, Circle’s transparent approach has helped it aggressively close the gap on Tether’s dominance.

Circle’s USDC is rapidly gaining market share due to a massive surge in institutional adoption and a broader industry shift toward regulatory safety. In the wake of high-profile crypto collapses, institutional investors and decentralized finance (DeFi) platforms are seeking stablecoins with highly liquid, verifiable reserves. Circle’s proactive compliance model, combined with strategic partnerships with major traditional financial institutions, has fueled its growth spurt and started to crack Tether’s long-standing monopoly.

Yes, while Tether (USDT) currently holds the top position by overall market capitalization, Circle (USDC) has a realistic path to overtaking it. USDC’s growth is heavily driven by its deep integration into the DeFi ecosystem and its status as the preferred digital dollar for Wall Street institutions. If global stablecoin legislation becomes stricter—such as the implementation of the MiCA framework in Europe or new US bills—Circle’s compliance-first infrastructure could accelerate its growth and ultimately flip Tether’s market dominance.

The intensifying competition between USDC and USDT creates a much healthier and more resilient cryptocurrency ecosystem. As Circle and Tether battle for the top spot, both issuers are pressured to improve their transparency, maintain safer reserve assets, and optimize cross-chain transaction fees. This shifting power balance benefits everyday users and institutions alike by providing safer digital dollar alternatives, reducing systemic risk, and ensuring highly stabilized liquidity across global crypto exchanges.