Subtotal $0.00

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by Themiya

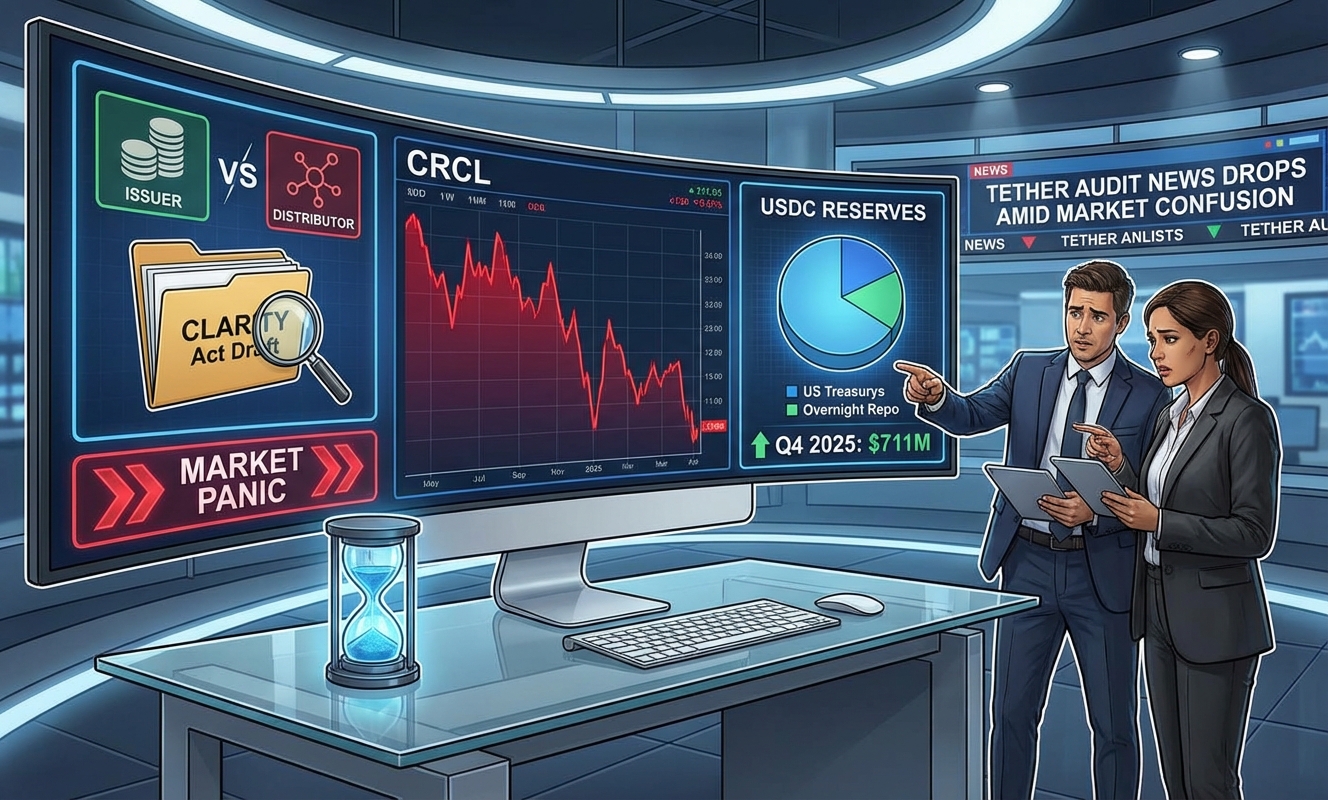

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by ThemiyaA 20% single-day crash. Five billion dollars in market cap vaporized. And it all happened on the same afternoon Tether decided to drop its Big Four audit news like a perfectly timed grenade. Coincidence? Maybe. But the crypto market rarely wastes a good opportunity to panic first and think later.

Let’s be real about what actually happened here. The CRCL selloff wasn’t a rational repricing of Circle’s business fundamentals. It was a knee-jerk reaction from traders who couldn’t distinguish between a stablecoin issuer and a stablecoin distributor. That’s a costly mistake, and some smart money is already betting on that confusion correcting itself.

Here’s the thing. The leaked CLARITY Act language banning passive stablecoin yield sent a cold shiver through a market that had already priced Circle for near-perfection. The stock had ripped 170% from its February lows, climbing from $50 to $127 on the back of earnings beats, USDC supply growth, and the assumption that Washington would play nice.

Then the draft landed. And the market lost its mind.

The new language would prohibit users from earning rewards just for holding a dollar-pegged token. Exchanges and affiliated platforms passing yield to customers, directly or indirectly, would be blocked too. Trading volume on CRCL exploded to 56.4 million shares. Nearly four times its 90-day average. That’s not organic selling. That’s algorithmic panic and forced liquidations doing their thing.

But here’s what everyone missed in the chaos. Circle doesn’t actually pay its users yield. That’s not its business model. At all.

The yield ban targets platforms passing income downstream to users. Think Coinbase, which currently offers around 3.5% on USDC balances and shares a chunk of that reserve income with Circle. That’s the target. Not Circle itself.

Bernstein analysts flagged this exact confusion in their post-selloff note. The market conflated the issuer with the distributor, punished the wrong entity, and created a dislocation. Cathie Wood’s ARK Invest spotted it immediately and bought 161,513 CRCL shares across three funds on the same day. $16.34 million worth. That’s not a speculative punt. That’s conviction buying on a mispriced asset.

Look, the timing of Tether’s Big Four audit announcement wasn’t accidental optics. Whether it was deliberate or just fortunate for Tether’s camp, the effect was the same. It landed right when Circle was already bleeding.

For years, Circle’s core positioning advantage in US and European institutional markets has been simple. It’s the “clean” stablecoin. Audited, regulated, compliant. Tether was always the offshore wild card with the sketchy reserves history. That positioning gap has been worth real money for Circle in terms of institutional adoption, banking partnerships, and regulatory goodwill.

If Tether actually completes a credible Big Four audit, that gap narrows. Significantly. Simon Dedic of Moonrock Capital put it bluntly: “The race between Tether and Circle just got a lot more interesting.” He’s right. And investors who had a premium baked into CRCL for that regulatory moat started questioning what that premium is actually worth now.

Honestly, this is the part of the selloff that deserves the most scrutiny. It’s not irrational. If Tether gets a clean audit and starts operating with transparent reserves, it competes directly in the institutional market Circle has been quietly dominating. That’s a real strategic threat, not a phantom one.

As if the day needed more fuel, Circle froze the USDC balances of 16 business hot wallets late Monday night. The freeze disrupted operations at exchanges, forex platforms, and casinos including FxPro, Pepperstone, AMarkets, and HeroFX.

The reason given? A US civil case with no disclosed details.

ZachXBT, who has spent years tracking on-chain fraud with more precision than most federal agencies, called it potentially “the single most incompetent freeze” he’d seen in five-plus years of investigations. His point was direct. Basic on-chain analysis would have shown these were active business wallets processing thousands of transactions. Legitimate commerce accounts. Not wallets tied to illicit activity.

This is the part that should genuinely concern long-term CRCL investors. Not the regulatory draft. Not Tether’s audit. This. Because it raises a real question about Circle’s internal compliance and freeze process. If the company is outsourcing freezing decisions to federal judges who apparently aren’t doing basic blockchain due diligence, that’s an operational risk that scale will only make worse. Freezing the wrong wallets once is a mistake. Doing it while the stock is in free fall is a communications catastrophe.

Strip away all the noise, and the USDC operating metrics haven’t blinked.

The Fed’s yield on reserves did drop from 4.49% to 3.81% between Q4 2024 and Q4 2025. That compression is a real headwind. But a 97% increase in average USDC supply over the same period more than compensated. Circle is essentially running a volume-over-margin playbook right now, and it’s working.

Bitwise CIO Matt Hougan’s take is worth noting here. He argued that Circle’s positioning in the stablecoin market gives it a structural advantage over the big banks that will eventually try to enter this space. His $75 billion valuation target for 2030 looks aggressive. But the directional logic isn’t wrong.

Bernstein has an Outperform rating and a $190 price target. Clear Street reiterated a Buy with a $152 target. The stock is currently trading around $104. That’s a lot of upside if the CLARITY Act language gets softened or narrowed during the legislative process, which, given how Washington works, is more likely than not.

Here’s the cynical read, and it’s the one I’d encourage you to sit with.

The CLARITY Act isn’t finished. Draft language leaks. Final bills look different. The OCC’s GENIUS Act implementation already pointed toward a world where payment stablecoin issuers can’t offer passive yield. This direction isn’t new. The market acted surprised by something the regulatory trajectory had been signaling for months.

But the real risk isn’t the yield ban. The real risk is a scenario where the legislation passes, Tether gets a clean audit, and traditional banks like JPMorgan or Bank of America launch their own FDIC-backed stablecoins with full deposit insurance. That’s a three-pronged squeeze. And Circle’s current moat gets meaningfully thinner under that scenario.

The Fed compression is also ongoing. If rates drop another 75 to 100 basis points over the next 12 months, Circle’s reserve income takes a direct hit unless USDC supply growth keeps accelerating to offset it. That’s an assumption worth stress-testing.

Don’t chase the bounce to $104. Wait and watch the CLARITY Act language closely over the next four to six weeks. If the final bill carves out clear exemptions for reserve-income-based business models (and it likely will, given industry lobbying pressure), that’s the entry signal. A move back toward $130 to $150 becomes very plausible on that catalyst alone. ARK’s $16 million dip buy is your tell. They’re not usually early by much.

References & Sources:

While Coinbase does not own Circle outright, the two cryptocurrency giants share a deep, symbiotic partnership. Coinbase is a vital backer and holds an equity stake in Circle, which is the primary issuer of the USDC stablecoin. A significant portion of Coinbase’s recent revenue is generated through this partnership, specifically from the interest yield earned on the fiat reserves backing USDC. Consequently, any regulatory shifts or financial setbacks hitting Circle—such as recent US rules restricting stablecoin reserve yields—can directly and heavily impact Coinbase’s bottom line.

Shares of Coinbase and other crypto companies have historically surged on favorable political and market shifts. Recently, upward stock momentum was fueled by political figures, including President Donald Trump, who signaled strong support for the cryptocurrency industry’s battle against traditional US banks regarding yield-bearing stablecoins. When combined with the broader momentum from Bitcoin’s price bounces, this type of high-level endorsement restores investor confidence and drives stock prices higher, even amidst complex regulatory environments.

The recent US regulatory rule has significantly impacted Circle’s market standing, effectively wiping an estimated $5 billion off its valuation. This strict framework places heavy constraints on how stablecoin issuers can manage their fiat-backed reserves and distribute yields. By restricting these yield-generating activities or mandating higher capital buffers, Circle’s profitability metrics are heavily squeezed. This immediate threat to their primary revenue engine caused a rapid decline in its implied valuation and raised operational concerns moving forward.

Even though the new US rule is aimed primarily at stablecoin issuers like Circle, the collateral financial damage to Coinbase could be far more severe. Coinbase relies heavily on the interest income generated from USDC reserves as a highly predictable revenue stream, which is absolutely crucial during periods of low crypto trading volume. If Circle is forced to alter its reserve management or cut the yield it shares with partners, Coinbase stands to lose a massive chunk of its quarterly revenue. Because Coinbase is a publicly traded company evaluated on continuous revenue growth, the stock market reaction to these lost earnings could result in a sharper, more visible financial blow to Coinbase than the private valuation hit taken by Circle.