Subtotal $0.00

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by Themiya

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by Themiya$1.156 billion in a single trading day. That’s what Strategy’s perpetual preferred stock, STRC, moved on April 13. Not Bitcoin. Not MSTR common stock. A preferred share instrument that most retail investors still don’t fully understand. And that’s exactly the problem.

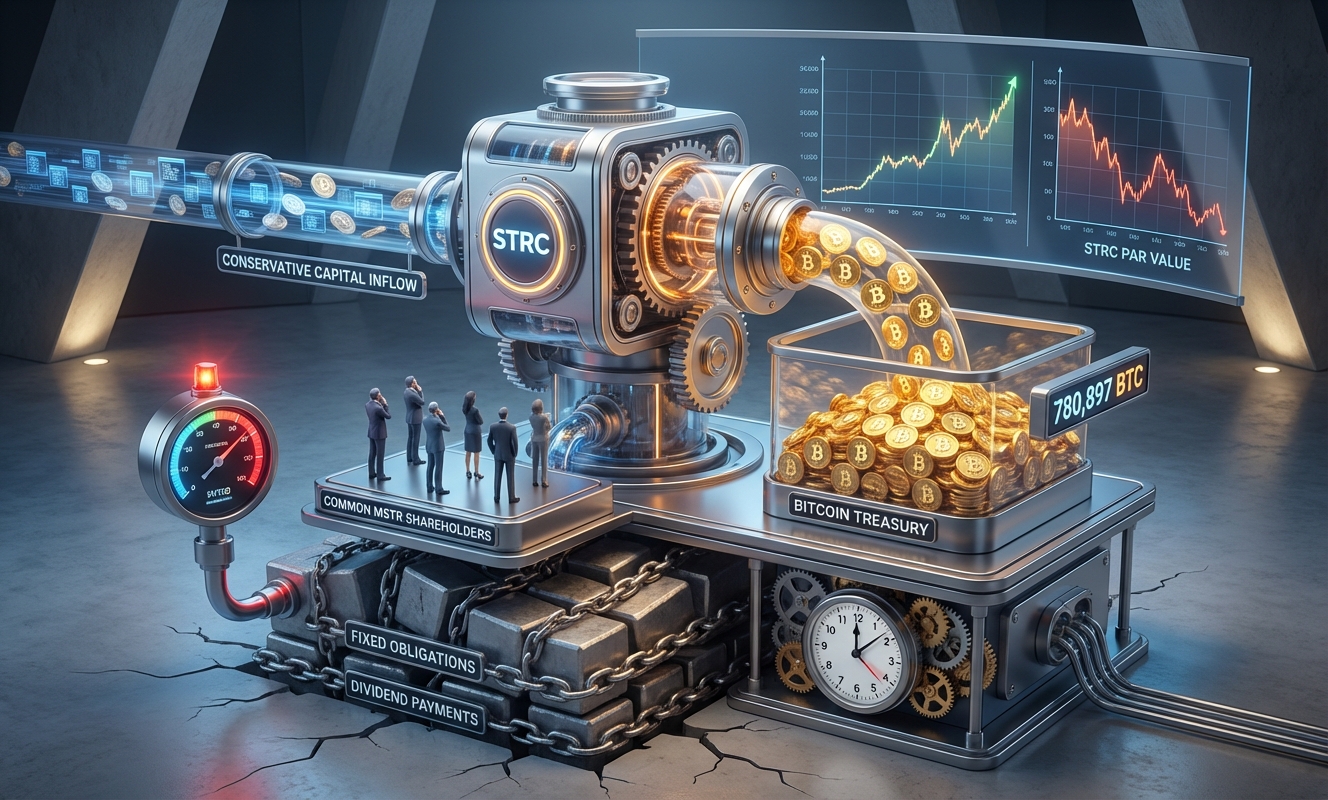

Let’s be real about what’s happening here. Strategy bought nearly 14,000 Bitcoin in one week, roughly $1 billion worth, and paid for every single satoshi using proceeds from STRC share sales. No common stock dilution. No debt raise. Just preferred stock, sold at a neat $100 par value, with an 11.50% annual dividend attached. Sounds clean. Almost too clean.

STRC launched in July 2025 with a very specific job. It needed to attract a class of investor that would never touch MSTR common stock: income-focused, low-volatility-seeking capital. Pension funds. Conservative allocators. People who want yield, not moonshots.

The structure is deliberately engineered to stay close to par. The adjustable dividend rate, currently sitting at 11.50%, acts as a pricing anchor. When STRC drifts below $100, the yield becomes attractive enough to pull buyers back in. When it rises above $100, sellers come out. It’s a self-correcting mechanism that gives Strategy an almost frictionless ATM (at-the-market) issuance program.

Here’s the thing most people miss. The genius isn’t the Bitcoin buying. The genius is who’s funding it. Strategy has effectively found a pool of conservative capital and redirected it into one of the most volatile assets on earth. The income investors get their yield. Strategy gets the Bitcoin upside. Common MSTR shareholders sit in between, hoping the whole structure holds together.

Saylor himself called it “money market-like stability with market-leading risk-adjusted returns.” That’s a bold pitch. Whether it holds up depends entirely on one variable: Bitcoin’s price trajectory.

Forget the marketing language for a second. Look at the actual architecture here.

Every time Strategy issues new STRC shares and converts the proceeds to Bitcoin, it adds another layer of fixed claims on top of the capital structure. Preferred stockholders get paid before common shareholders. Always. That’s the legal reality of how preferred equity works.

Strategy’s underlying software business doesn’t generate anywhere near enough operating cash flow to cover these dividend obligations. So in February, the company built a $2.25 billion reserve, essentially a dedicated war chest designed to cover roughly two and a half years of preferred dividends and debt interest. That sounds like prudent risk management. And it is, if everything goes according to plan.

Honestly, the reserve only buys time. It doesn’t fix the structural dependency on continuous market access.

Supporters argue the math works as long as Bitcoin keeps climbing. Saylor has stated Strategy’s BTC breakeven ARR (Accounting Rate of Return) sits at approximately 2.05%. If Bitcoin compounds above that rate, the company can theoretically service preferred dividends indefinitely without touching new MSTR common share issuance.

Analyst Adam Livingston framed it well. Each STRC issuance, in his view, converts capital markets access into long-duration Bitcoin exposure, while the fixed preferred claim shrinks in relative importance as BTC’s asset base grows. The fixed obligation stays the same in dollar terms. The Bitcoin underneath appreciates. Net result: the preferred stack becomes a smaller and smaller burden relative to total assets.

It’s a compelling thesis. It’s also completely dependent on Bitcoin not having a prolonged bear market at the exact moment Strategy needs to refinance or service obligations.

This is where independent analyst Derin Olenik comes in, and his numbers are worth taking seriously.

Olenik calculated that STRC obligations are growing at a compound monthly rate of roughly 30%. At that pace, total obligations could increase tenfold within a year. His core warning: Strategy could burn through its $2.25 billion reserve in nine to ten months, not the projected two and a half years.

The scenario that should make MSTR common shareholders genuinely uncomfortable is this one. If ATM issuance slows or stops, Bitcoin accumulation stops with it. But if issuance continues at the current pace, the dilution math becomes brutal. Olenik’s calculations suggest that even if MSTR stock returns to all-time highs, Strategy may need to issue over one billion new shares to cover preferred dividends, representing nearly 400% dilution of existing common equity.

He didn’t mince words about it, calling STRC “Digital Kamikaze” from a common shareholder perspective. That’s not a fringe view. It’s a structural critique based on the company’s own financial disclosures.

Here’s where it gets interesting for the broader market. Strategy now holds 780,897 Bitcoin at an average cost of $75,577 per coin. That’s a $59 billion position funded significantly by financial instruments that carry fixed obligations.

If Strategy ever faces a liquidity crunch, the forced selling pressure on Bitcoin would be significant. We’re not talking about a whale dumping bags quietly. We’re talking about a corporate treasury event that would almost certainly move markets. The crypto market would see it coming, which means front-running would amplify any downward move.

On the flip side, as long as this machine keeps running, Strategy is a guaranteed consistent buyer of Bitcoin. Every successful STRC raise translates directly into BTC purchases. With $21.6 billion in authorized STRC shares still available, the potential buying pressure is not trivial. That’s structurally bullish for Bitcoin price support, at least in the near term.

The entire STRC model is predicated on continuous capital markets access at or near par. That assumption holds in a benign rate environment where income investors are hungry for yield. But what happens when it doesn’t?

Think about what a genuine credit crunch or a spike in risk-free rates does to this instrument. Suddenly, 11.50% doesn’t look as attractive relative to alternatives. Demand for new STRC shares falls. The ATM program slows. Bitcoin accumulation stops. The reserve starts bleeding faster than projected. And here’s the kicker: the preferred dividend obligations don’t stop just because the ATM program does.

Strategy’s own risk disclosures acknowledge this plainly. Future preferred issuance could dilute existing shareholders and adverse shifts in financing conditions could make it harder to maintain dividend reserves. That’s the company telling you, in legal language, that this structure has a breaking point. The question is just whether Bitcoin’s appreciation outpaces the structural deterioration fast enough.

Between you and me, betting that a company whose software division can’t cover its own dividend obligations will perfectly time Bitcoin appreciation cycles for the next decade is a very specific kind of faith. Some call it vision. Others call it a leveraged bet dressed up in capital markets language.

Pro-Tip: If you hold MSTR common stock, the metric to watch isn’t Bitcoin’s price alone. Watch the spread between STRC’s market price and its $100 par value. If STRC starts trading at a persistent discount to par, it signals that demand for new issuance is weakening. That’s your early warning system for when the ATM machine starts to stutter. A discount of even two or three percent would fundamentally change the economics of Strategy’s entire accumulation model, and you’d want to know about it before the quarterly report confirms it.

References & Sources:

Strategy, formerly known as MicroStrategy, largely funds its massive Bitcoin acquisitions through the capital markets. According to regulatory filings, a significant portion of these purchases is funded through the strategic sale of Class A common stock. This fundraising method allows the company to continuously expand its Bitcoin treasury—enabling monumental moves like their recent $1 billion acquisition—while preserving operational cash flow.

According to Executive Chairman Michael Saylor, concerns that Strategy might be forced to sell its Bitcoin during a market downturn are completely unfounded. The company maintains a remarkably stable capital structure, boasting a net leverage ratio that is half that of a typical investment-grade company. This strong financial foundation ensures that Strategy can comfortably weather crypto market volatility and hold its Bitcoin reserves for the long term without facing forced liquidation.

Yes, Michael Saylor’s Strategy Inc. successfully acquired nearly $1 billion in Bitcoin for a second consecutive week. By capitalizing on recent cryptocurrency price pullbacks, the company aggressively added to its digital asset portfolio. This relentless accumulation strategy is a major catalyst behind the intense market enthusiasm, driving STRC to record trading volumes and causing its market cap to double since Friday.

Strategy’s STRC stock reached record trading volumes largely due to investor excitement surrounding its latest massive $1 billion Bitcoin purchase. As the company aggressively expands its cryptocurrency holdings, investor confidence has skyrocketed, resulting in a surge of institutional and retail trading activity. This historic buying spree not only broke volume records but also caused the company’s market capitalization to double in a matter of days.