Subtotal $0.00

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

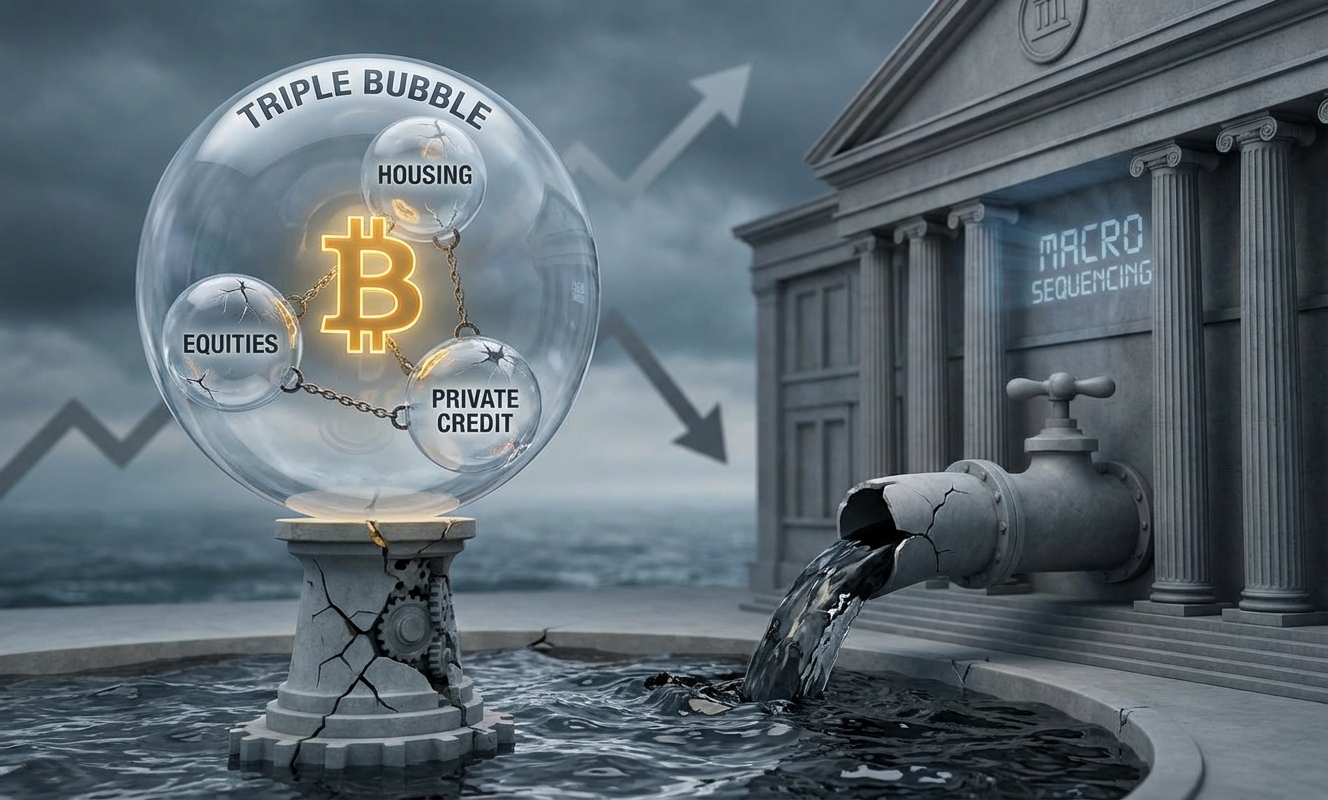

Nobody rings a bell at the top. But right now, three separate asset markets are priced for perfection simultaneously, and Bitcoin sits directly in the blast radius of whichever one cracks first.

Let’s be real about what’s happening. This isn’t a Bitcoin story. Not yet. It’s a macro sequencing story, and Bitcoin just happens to be the most liquid, 24/7, no-circuit-breaker asset on the planet. That makes it the first thing institutions sell when they need cash, and the first thing they chase when the Fed opens the liquidity spigot. You need to understand that duality before you touch a single position right now.

Macro strategist Michael Pento coined it. Equities near historic valuation extremes, housing locked up by mortgage rates sitting at 6%, and private credit ballooning toward $2 trillion in assets under management. Three separate pockets of stretched valuations, each with its own fragility.

Here’s the thing: the label isn’t the point. The sequencing is.

Systems don’t break because valuations look uncomfortable on a chart. They break when credit and bond market plumbing forces involuntary selling. Think of it like a house of cards. The cards can look precarious for months. What finally knocks it over is someone pulling a specific card from the bottom row.

That third scenario, honestly, is the most underappreciated risk right now.

Look at the indicators without the narrative spin:

Read that last point again. Nearly half of peak leverage has already been flushed. That’s not nothing. It reduces the immediate risk of a cascade liquidation spiral. But it also means if fresh stress arrives, there’s still room for forced selling to resume, because the underlying macro conditions that caused the deleveraging haven’t resolved.

The market is literally sitting in a waiting room right now.

Bitcoin collapsed nearly 40% on a single day in March 2020. Straight down. No warning. Perpetual funding went deeply negative, open interest imploded, and stablecoin supply contracted as people raced for dollar liquidity. It was ugly.

Then the Fed cut to zero, launched unlimited QE, and stood up emergency lending facilities. Within weeks. Bitcoin recovered from that March 12th low and quintupled over the next year.

The retail read: “Bitcoin always recovers, so buy the dip.”

The actual lesson: Bitcoin’s behavior is almost entirely downstream of Fed liquidity decisions. The asset itself didn’t change between March and April 2020. What changed was the real yield environment and the speed of dollar liquidity injection.

March 2023 reinforces this. Banking sector stress hit. Bitcoin rose 26% in a week, roughly 40% in 10 days, front-running the Fed’s liquidity response before traditional assets even stabilized. That’s the high-beta rescue trade in action.

February 2026 showed the same reflex: Bitcoin whipped from $60,000 to above $70,000 in a single day. Its largest one-day move since March 2023. Pure macro sentiment repricing.

This is the part that doesn’t get enough attention in crypto circles. Moody’s expects private credit AUM to surpass $2 trillion in 2026 and approach $4 trillion by 2030. Bank of America has committed $25 billion to the space. Structural growth, sure. But also structural opacity.

Private credit sits in less-transparent structures. Longer lockups. Weaker covenant protections. When these portfolios face stress, they can’t sell their underlying assets quickly. So what do they sell? Liquid public market assets. Through collateral calls and margin pressure.

Bitcoin, as the most liquid 24/7 asset on earth, absorbs that selling disproportionately. This is not speculation. This is basic portfolio plumbing mechanics.

The 2020 analog is instructive, but private credit wasn’t $2 trillion in 2020. The potential contagion vector is larger now. And it’s less visible until it isn’t.

Stop looking at price. Seriously. At this stage, price is the last thing to react. Track these instead:

On the crypto-native side, watch perpetual funding rates for sign reversals, open interest trends for rebuilding leverage (a rescue signal) versus continued collapse (liquidation), and ETF flow direction over multi-week windows, not single-day noise.

Around 206%. Highest level ever recorded, according to Advisor Perspectives. Freddie Mac’s 30-year fixed mortgage rate is still sitting at 6.01%.

These aren’t direct Bitcoin triggers. They’re amplifiers. When equity valuations are this stretched and credit eventually does crack, the correction magnitude is larger because there’s less cushion. Multiple compression hits harder from 206% than from 150%.

Bitcoin doesn’t care about the Buffett indicator on a Tuesday afternoon. But if equities correct 20-30% from these levels because earnings fail to justify multiples, Bitcoin will not be a safe haven in the acute phase. It will sell off first. It always does.

Here’s the scenario that ends careers. Inflation stays sticky above 3%. Bond markets demand higher term premiums to compensate for fiscal risk. Real yields stay elevated at 1.8% or above. And credit stress builds slowly rather than fracturing in a clean, visible event.

In this environment, the Fed can’t rescue quickly without reigniting inflation. The “buy Bitcoin because dollar debasement” narrative competes directly with “sell Bitcoin because real yields are too high.” Both theses are simultaneously true. The market chops violently in both directions.

This isn’t a theoretical risk. The 10-year TIPS at 1.80% with core inflation still above 2.5% is basically that regime right now. The catalyst for either clean resolution, full credit fracture or decisive Fed pivot, hasn’t arrived yet.

Between you and me, the market is being kept afloat right now by the absence of a trigger, not the presence of genuine fundamental strength.

If you’re positioning for the next major Bitcoin move, build a simple weekly dashboard. Not a price chart. A macro plumbing chart.

The worst trade you can make right now is maximum leverage long because “Bitcoin always recovers.” It does. But it can cut you in half on the way to doing so. And at 1.80% real yields with $4.3 billion in ETF outflows over five weeks, the burden of proof for a new bull leg is on the bulls.

Macro sequencing decides the outcome. Not your thesis. Not the halving cycle narrative. Not the next ETF filing. Credit breaks or it doesn’t. The Fed rescues or it doesn’t. Everything else is noise.