Subtotal $0.00

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by Themiya

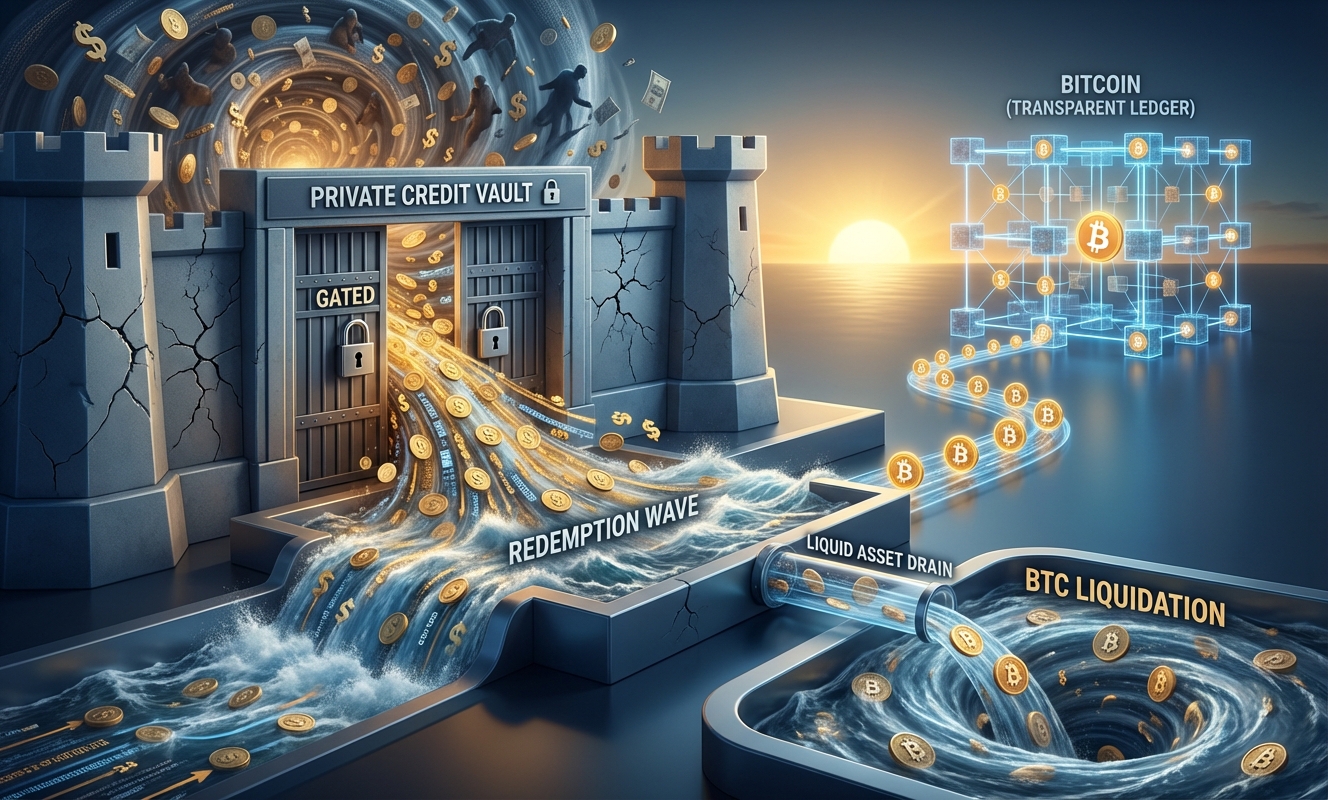

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by ThemiyaThe gates are closing. Not at some obscure micro-fund nobody’s heard of. At Barings. At Apollo. At Ares. At Blue Owl. The biggest names in private credit are quietly capping withdrawals while tens of billions in investor cash is lined up, knocking on a door that won’t fully open. That’s not a coincidence. That’s a structural crack running through a $3 trillion market, and crypto investors who think this is somebody else’s problem are about to get a very expensive education.

Let’s be real about what’s actually happening here. In Q1 2026, investors tried to pull over $20 billion from private credit funds. The Financial Times confirmed it. The Wall Street Journal confirmed it. The numbers from individual managers are almost comically consistent: Barings hit a 11.3% redemption request, Apollo saw 11.2%, Ares got slapped with 11.6%. Blue Owl is the one that should genuinely alarm you, investors tried to exit 21.9% of Blue Owl Credit Income Corp. and a staggering 40.7% of Blue Owl Technology Income Corp.

Both funds capped repurchases at 5%.

Think about that math for a second. Someone wanted 40 cents on every dollar back. They got 5 cents. The rest? Locked inside a structure that is now working exactly as designed, which is the problem nobody selling these products ever wanted to discuss openly.

Here’s the thing about private credit’s explosive growth over the last decade. It wasn’t built on superior returns alone. It was built on a sales pitch with a very convenient blind spot baked into it.

The model worked beautifully. Right up until it didn’t. Because the entire architecture depends on one critical assumption: that not enough investors panic at the same time. When that assumption breaks, the gates aren’t a feature. They’re an admission.

Redemption caps alone? Manageable optics. Redemption caps plus a Moody’s negative outlook on Blue Owl Credit Income and a sector-wide negative outlook on BDCs? That’s a different category of problem.

Ratings agencies move slowly. Deliberately slowly. When Moody’s shifts an entire sector’s outlook to negative, it’s not reacting to one bad quarter. It’s signaling that the structural vulnerabilities are now visible enough that they can no longer be treated as internal fund-management noise. Flow stress, asset quality concerns, rising financing costs, and collapsing confidence are now sitting in the same frame at the same time.

Honestly, that sequencing matters more than any individual data point. Redemption waves first. Gates second. Ratings pressure third. The next step in that chain is secondary market pricing forcing NAV assumptions into the open, and Sycamore Tree Capital’s launch of a private-credit secondary strategy tells you sophisticated money already sees that coming.

Mercer Capital flagged it plainly: public BDC discounts are beginning to signal a disconnect between public pricing and private NAV assumptions. Translation? The same underlying credit exposure is being priced materially cheaper in public markets than private fund managers are reporting in their quarterly marks.

That gap is essentially free money for anyone willing to exit the private wrapper, take the haircut from the secondary market, and re-enter the exposure through public vehicles trading at a discount. Once enough investors figure that out, the incentive to stay locked inside private fund structures deteriorates fast. The secondary market doesn’t fix the problem. It accelerates price discovery in a way that makes comfortable manager marks impossible to defend.

Jamie Dimon said it this week, carefully and with all the diplomatic hedging you’d expect from someone running JPMorgan. Weaker lending standards. Optimistic assumptions. Losses potentially larger than expected. That’s as close as establishment banking gets to saying “we helped build something fragile.”

Crypto Twitter wants a clean narrative here. “Private credit implodes, capital floods into Bitcoin.” Look, it’s more complicated than that, and pretending otherwise is just shilling with extra steps.

In the first phase of a real credit shock, liquid assets get sold first. Always. When a fund manager faces redemption pressure and can’t easily sell illiquid loans, they sell whatever they can. Equities. ETFs. Bitcoin. The same 24/7 liquidity that makes BTC attractive in normal markets makes it the first exit ramp in a panic. We’ve seen this movie before.

If private credit stress accelerates into Q2 and forces broader risk-off positioning across institutional portfolios, Bitcoin is not a safe haven in that moment. It’s exit liquidity for someone else’s problem.

Here’s where it gets genuinely interesting. If private credit spends the next several quarters proving that opaque pricing, gated access, and manager-controlled valuations are features that benefit the manager more than the investor, capital starts asking harder questions about every asset class that relies on the same architecture.

That contrast becomes valuable narrative capital during a prolonged credit cycle that keeps exposing the gap between reported stability and actual liquidity. It won’t happen in a straight line. It won’t be immediate. But the long-term capital rotation thesis for Bitcoin gets meaningfully stronger every time a gated fund demonstrates that the “smooth returns” were always partially an accounting choice.

This is the part that doesn’t get enough attention. Private credit isn’t just a product for sophisticated institutional allocators anymore. Distribution has broadened dramatically, and there are still active proposals to push private-market exposure deeper into retirement accounts and pension-adjacent channels.

Think about that timing. A market actively discovering the hard limits of its own liquidity, simultaneously arguing it should have wider access to retirement savings. That’s a regulatory and political disaster waiting to happen. Once lockups and losses become visible to a broader, less sophisticated investor base, the reputational and legal fallout will be significant. And that fallout will reshape how regulators think about all alternative asset structures, including crypto products, for years.

The assets are different. The vehicles are different. The borrowers are different. Fine. But the core vulnerability is identical: illiquid assets, funded through structures promising periodic liquidity, distributed to investors who didn’t fully model what “illiquid” means under stress. The mechanism for confidence collapse is the same. Enough investors try to leave at once, the structure can’t accommodate them, the gap between reported value and realizable value becomes undeniable, and confidence in the marks poisons the whole category.

That cycle hasn’t completed yet. The data doesn’t support calling this a full systemic break right now. But the pathway to one is clearer than it was 90 days ago, and the market has identified exactly where the confidence can fail. That’s important information regardless of whether the worst-case outcome actually materializes.

Here’s your risk factor, and I mean this seriously: don’t front-run the flight to Bitcoin on this thesis without understanding the two-phase dynamic.

Phase one of a private credit dislocation is bearish for BTC. Forced selling hits liquid assets first. If Q2 redemption data comes in worse than Q1 and ratings pressure spreads beyond Blue Owl, expect correlated selling across risk assets including crypto. The people managing these funds will be scrambling for cash, and BTC is cash in a way that illiquid loans simply aren’t.

Phase two, the structural repricing of trust and transparency, is a multi-quarter or multi-year thesis. It requires the private credit narrative to keep deteriorating publicly. It requires secondaries to force real price discovery. It requires retail-adjacent investors to feel genuinely burned by gated structures they didn’t fully understand.

If you’re a long-term holder, this macro backdrop strengthens the case for Bitcoin’s comparative transparency. If you’re a short-term trader, watch the Q2 redemption data from Barings, Apollo, Ares, and Blue Owl like a hawk. That data will tell you whether this is contained or whether the self-reinforcing cycle (gates driving skepticism, skepticism driving more redemptions, more redemptions forcing asset sales) is now in motion.

The private credit market has moved decisively out of its confidence phase. What comes next depends on whether managers can restore trust before the loans themselves need to be repriced in public. Right now, the evidence says that’s a very difficult ask.

References & Sources:

The looming Wall Street private credit crisis is being primarily driven by a massive $20 billion wave of investor exit requests. As high-net-worth individuals and institutional investors seek to cash out of illiquid private credit funds, fund managers are being forced to impose strict withdrawal limits. This liquidity crunch is exacerbated by higher interest rates, rising default risks among borrowers, and a general tightening of macroeconomic conditions, leaving funds struggling to meet redemption demands without selling assets at steep discounts.

When private credit funds impose withdrawal limits—often referred to as “gating”—it traps investor capital and drastically reduces overall market liquidity. This forces institutional investors to liquidate other, more liquid assets to meet their immediate cash flow needs or margin requirements. Consequently, the forced sell-off can spill over into public equities, bonds, and alternative markets, creating a domino effect that increases market-wide volatility and depresses asset prices across the broader financial ecosystem.

The $20 billion exit wave in private credit threatens Bitcoin liquidity due to the interconnected nature of modern institutional portfolios. As investors find their capital locked up in traditional private funds due to sudden withdrawal limits, they are increasingly forced to sell highly liquid alternative assets, like Bitcoin, to raise necessary cash. This sudden, forced selling pressure in the cryptocurrency market can quickly drain Bitcoin’s order book liquidity, leading to sharp price corrections and amplified volatility.

Key warning signs of a private credit fund facing a liquidity crisis include the sudden implementation or extension of withdrawal limits (gating), delays in scheduled dividend distributions, and the forced sale of prime portfolio assets at distressed prices. Additionally, if a fund rapidly increases its internal borrowing to meet redemption requests or shifts its valuation metrics to mask underlying losses, it strongly indicates that the fund is struggling with a severe imbalance between illiquid loan assets and a rush of investor exit demands.