Subtotal $0.00

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Magazines cover a wide array subjects, including but not limited to fashion, lifestyle, health, politics, business, Entertainment, sports, science,

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by Themiya

Fact Checked by Coinsbeat Editorial Team | Expert Reviewed by ThemiyaWashington just handed the stablecoin market a yield ban. And somehow, the money is still flowing. It’s just flowing to everyone except you.

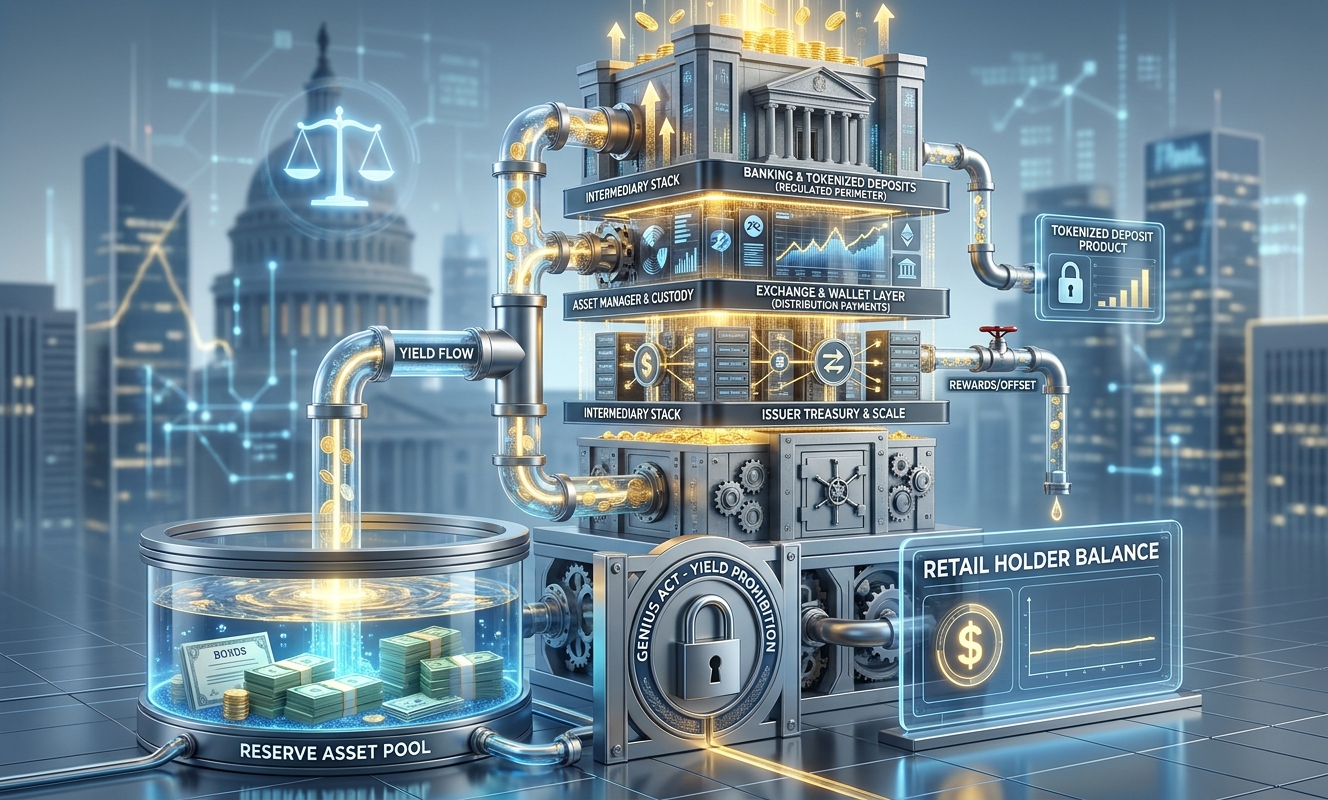

The GENIUS Act is clear on paper: payment stablecoin issuers cannot pay holders interest or yield for simply holding, using, or retaining a stablecoin. Clean prohibition. Simple language. Except the $320 billion stablecoin market doesn’t run on simple language. It runs on reserve income, distribution agreements, platform balances, and custody fees. And none of those stop existing just because a statute says holders can’t get a direct cut.

This is the part most coverage skips. The yield didn’t disappear. It got redistributed upward.

Let’s be real about what a stablecoin actually is under GENIUS. It’s a regulated cash-management product backed 1:1 by reserves that include short-term Treasuries, bank deposits, repo arrangements, and government money market funds. Those assets generate income. Real, meaningful income.

Tether’s market cap is sitting at roughly $189.7 billion. USDC is around $77.6 billion. Plug even a modest Treasury yield into those numbers and you’re talking about billions of dollars annually in reserve income. The statute says the issuer can’t hand that back to holders directly. It says absolutely nothing about what happens before the money gets anywhere near a holder.

Circle’s S-1/A filing lays this out with almost uncomfortable specificity. There’s an issuer portion. There are allocations tied to stablecoins held in Coinbase custodial products or managed wallets. Then Coinbase receives 50% of the remaining payment base after approved participant payments. Coinbase’s own 10-K calculated that a 150 basis-point rate move on daily USDC reserve balances would swing stablecoin revenue by $540 million for 2025 alone.

Read that number again. $540 million. From one rate sensitivity calculation. On one stablecoin. At one exchange.

The holder sees a stable dollar. The intermediary stack sees a yield-generating machine with the consumer systematically cut out of the economics.

Here’s the thing most retail participants don’t grasp. The GENIUS Act didn’t flatten the economic landscape. It just defined the battlefield. And that battlefield now runs through every party sitting between the reserve asset and your wallet.

PayPal’s July 2025 announcement tells you exactly how this repackaging works commercially. Instant crypto-to-stablecoin conversion. A 0.99% merchant transaction rate. PYUSD rewards for funds held on-platform. That is not a yield product. That is a payment product with yield-shaped incentives carefully distributed across the merchant relationship, the conversion spread, and the rewards structure. Legally different. Economically, pretty similar from where you’re sitting.

The Bank Policy Institute isn’t fighting this battle out of principle. They’re fighting it because they understand the money map. Their August 2025 argument was straightforward: if exchanges and distribution partners can still effectively pay indirect yield on stablecoins, GENIUS’s issuer ban is economically hollow. The deposit-flight risk remains. The credit-creation argument weakens.

Honestly, that argument isn’t wrong on the mechanics. It’s just self-serving in the conclusion.

The crypto trade groups fired back with the predictable counter: third-party rewards are competitive consumer benefits, not statutory evasion. Both positions have merit. Both positions are also covering economic interests with legal language.

The FDIC’s April 7 proposal adds another wrinkle. Qualifying tokenized deposits get treated as deposits under the Federal Deposit Insurance Act. Full stop. That gives banks a structurally cleaner path. If stablecoin rewards get legislated into a corner by CLARITY’s final text, banks can offer tokenized deposit products that keep the interest economics inside the regulated deposit framework. Banks win that scenario. Stablecoin-native platforms lose distribution leverage.

JPMorgan has been saying for months that global regulators favor tokenized bank deposits over stablecoins. Look at the FDIC proposal and it’s hard to argue they’re wrong about the regulatory trajectory, even if the market hasn’t fully priced it.

Look, the White House dropped a note on April 8 that was supposed to defend the yield prohibition. It estimated a $2.1 billion increase in bank lending from eliminating stablecoin yield. That’s a 0.02% lending effect. Against an $800 million net welfare cost to consumers.

The administration published its own argument and it came out looking shaky. The lending boost is trivially small. The consumer welfare drag is real and measurable. And the same note acknowledged that affiliate and third-party arrangements could remain open unless CLARITY explicitly closes them.

So the policy produces a marginal bank lending benefit, a concrete consumer cost, and a half-open loophole. That’s not a strong trade-off. It’s a compromise that satisfied enough lobbying pressure to pass while leaving the actual economic redistribution question unresolved. Washington being Washington.

The CLARITY vote is the critical variable. Two outcomes dominate the distribution of stablecoin economics going forward.

If third-party rewards survive CLARITY intact, platforms with large user bases, deep distribution, and existing issuer relationships win enormously. Coinbase, PayPal, and whoever owns the dominant wallet stack in the next cycle will capture stablecoin economics that holders can’t access directly. Market concentration increases. Smaller platforms without issuer relationships get squeezed out of the distribution economics entirely. Expect further vertical integration.

If CLARITY closes the third-party channel, bank tokenized deposit products gain structural advantage overnight. The economics migrate into the regulated deposit perimeter. Traditional finance infrastructure becomes the dominant stablecoin distribution layer. USDe, PYUSD, and non-bank stablecoin issuers face a harder climb. USDT’s offshore positioning gets even more complicated for compliant institutional holders.

Either way, the $320 billion stablecoin market’s yield economics are being fought over by parties who are not retail holders. The retail holder is mostly a source of balance float in this equation. That’s worth understanding clearly before you decide what position to hold and where to hold it.

Let’s be blunt. If you’re holding USDC on Coinbase and thinking you’re getting the full benefit of a dollar-denominated asset in a high-rate environment, you’re not. You’re providing balance float that Circle and Coinbase split on a 50/50 basis after expenses. The yield lands in their revenue lines. Your 10-K looks nothing like theirs on this question.

The risk factors worth watching right now:

The pro-tip here is straightforward. If you’re using stablecoins and you want any part of the yield economics that your balances generate, look at protocols operating outside the GENIUS payment stablecoin definition. USDe at $3.79 billion is structured around delta-neutral collateral strategies that generate native yield without being a “payment stablecoin” under the statute. The regulatory risk there is different but the economic access is different too. Understand what you own before assuming a dollar is just a dollar.

The GENIUS Act didn’t kill stablecoin yield. It just decided who gets to keep it. Spoiler: it’s not you.

References & Sources:

The “9 banks stablecoin” refers to an initiative driven by Qivalis, a joint venture formed by a consortium of nine major European banks: Banca Sella, CaixaBank, Danske Bank, DekaBank, ING, KBC, Raiffeisen Bank International, SEB, and UniCredit. Announced in September 2025, this powerful banking alliance aims to launch a MiCAR-compliant, euro-pegged stablecoin in the second half of 2026 under the supervision of the Dutch Central Bank (DNB). This massive move illustrates how traditional financial heavyweights are aggressively entering the blockchain space to compete with private issuers, aiming to capture the transactional power and reserve yield inherent in digital currency economics.

The CLARITY Act is a highly anticipated U.S. market-structure proposal aimed at establishing clear regulatory frameworks for cryptocurrency assets. The legislation clarifies whether the Securities and Exchange Commission (SEC) or the Commodity Futures Trading Commission (CFTC) has oversight by categorizing digital assets into three primary buckets: digital commodities (like Bitcoin), investment contract assets (such as tokens sold via ICOs), and payment stablecoins (like USDC or PYUSD). By formally defining fiat-backed payment stablecoins, the CLARITY Act lays the regulatory groundwork for a monumental shift, deciding which entities—banks, crypto-native firms, or tech platforms—have the legal backing to capture the economics of the digital U.S. dollar.

Historically, the primary fight in the stablecoin sector was about who gets to keep the massive yields generated by the traditional fiat reserves—such as high-interest U.S. Treasury bills—backing the tokens. However, with the introduction of the CLARITY Act, the battleground is evolving. The focus is shifting toward “digital-dollar economics,” which involves controlling the core infrastructure of global digital payments. Stakeholders are realizing that capturing market share, user transaction fees, network lock-in, and the geopolitical advantage of running the digital rails for the U.S. dollar presents a far more lucrative and long-lasting economic opportunity than merely harvesting short-term interest yields.

The CLARITY Act will drastically reshape the competitive landscape for stablecoin issuers by introducing strict federal guidelines, reserve requirements, and consumer protection mandates. For incumbent crypto-native issuers like Circle (USDC) and Tether (USDT), it means adhering to rigorous new compliance structures to maintain their dominance. Concurrently, the Act provides the regulatory certainty that traditional banks and massive fintech companies have been waiting for. This clear legal runway empowers traditional financial institutions to mint their own digital dollars, intensifying the battle over who will ultimately control and profit from the future of tokenized global finance.